How to Actually Build Wealth and Retire Early (Explained in 6 Minutes)

I started my journey four years ago with $1,000 as a student, and built a portfolio that now generates enough returns for me to live off. Along the way, I saw many people make exceptional returns. But also many who lost it all again.

This is not a “get rich quick” article, but rather a guide on how to build wealth safely and sustainably over the long term.

Many people think building wealth is about:

It's not.

1. Understanding the core principle

Building wealth is about owning productive assets over a long period of time.

Stocks, real estate, precious metals, crypto… all of this sounds very complicated. But fortunately, the most effective way to build wealth is also the easiest one.

The holy grail is the stock market, more specifically index funds (ETFs). For those new to investing: ETFs let you invest in entire categories rather than individual stocks. For example, you can invest in the entire energy sector instead of picking individual energy stocks.

I will keep this as simple as possible. Your goal is to invest as diversely as possible in order to capture the broader market return and avoid concentration risk in your portfolio. The simplest way to do this is by investing in an All-World ETF, which essentially covers the entire stock market.

The internet is full of stock tips and people claiming they can beat the market. The reality is that fewer than 10% of hedge funds manage to outperform the market over a 20-year period. And we are talking about billion-dollar funds with analyst teams working around the clock.

Even if you could theoretically outperform the market over the long term (which you can’t), taxes still exist. They make a passive buy-and-hold strategy far superior. Holding an ETF for decades and deferring taxes until sale allows compound interest to work in your favor.

Active trading and constantly rotating individual stocks would destroy your returns in most countries purely because of taxes. More on that in the next section.

2. Compound interest

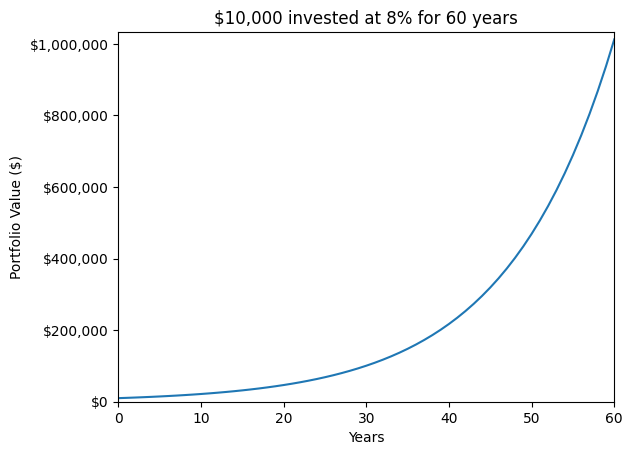

Your expected return with this strategy is historically around 8% per year. That does not sound like much at first glance, until you factor in compound interest. As a simple rule of thumb, your money roughly doubles every 10 years.

$10 invested today becomes:

After 40 years, you have already multiplied your money by sixteen.

This chart visualizes it even better. $10,000 invested today at an 8% annual return grows to just over $1,000,000 after 60 years. Of course, $1,000,000 in 60 years will not have the same purchasing power as today. But for the sake of simplicity, we are ignoring inflation here.

3. When to start investing?

Now. Your goal is not to wait for the perfect entry, but to stay invested in the market for as long as possible. I am aware that many people are afraid to invest at all-time highs.

The following chart illustrates very well why this fear is unjustified. The green dots mark when the S&P 500 reached a new all-time high. If investing at one of these points scares you, it will likely cost you a lot of returns.

In fact, the S&P 500 reaches a new all-time high on roughly 8% of all trading days.

If you have a lot of money that you want to invest, it’s understandable that you don’t want to put it all into the market at once. Even though lump-sum investing is statistically superior, it’s emotionally understandable and totally justifiable to dollar-cost average into the market over two to three years.

4. Asset allocation

What other assets should you buy?

In general, ETFs should make up the majority of your portfolio. It depends somewhat on the size of your portfolio, but I would say 70-80% is a reasonable lower bound. As your portfolio grows, it makes more sense to diversify into other asset classes.

Crypto makes little sense for most people. The only exception is Bitcoin, where I consider an allocation of 2-5% reasonable. This may sound strange coming from someone who made their money through crypto trading, but it is important to clearly distinguish between investing and active trading.

It is a niche where you can make a lot of money by exploiting market inefficiencies. But unless you do this professionally, you’ll most likely end up losing money.

Real estate is complex and highly individual, depending on where you live.

Buying makes sense in two scenarios:

Otherwise, you will not beat stock market returns and you will have significantly more work on top of that.

Precious metals belong in a long-term portfolio. But the same principle applies here. If your portfolio is still small, you do not need them. Once your portfolio reaches a certain size, diversification becomes more important. Around 10% in gold and silver is a reasonable guideline.

5. Retirement

At what point can you retire?

Let’s assume your portfolio is 100% invested in ETFs. It’s not enough to simply say that the 8% expected return needs to cover your expenses because returns are not evenly distributed over time.

Market fluctuations mean that during crashes, you are forced to withdraw more than 8% of your portfolio. Over time, this can cause your portfolio to shrink, even if your average return remains 8%. If you want to learn more about this, you can look up “sequence of returns risk.”

A commonly used rule of thumb is the 4% rule. It states that you can withdraw around 4% of your portfolio each year with a high probability of not running out of money over time. To calculate how large your portfolio needs to be in order to live off the returns, you can simply take your monthly expenses and multiply them by 300.

Example (assuming you want to live on $6,000 per month):

$6,000 × 300 = $1,800,000

→ With a portfolio of $1,800,000, you could comfortably withdraw $6,000 per month and live off it.

The goal shouldn’t be to retire as fast as possible. It’s much more about understanding how to use time and compound interest to your advantage. Starting as early as possible is crucial, and even small savings rates make a huge difference over time.

If this article was helpful to you, I’d really appreciate a like, retweet, and comment to support the algorithm. And feel free to follow me @onchainmo for all kinds of content around finance and investing, with a particular focus on crypto.

Disclaimer: This is not financial advice. I’m not a financial advisor. This article reflects my personal experience and opinions.